2QFY2019 Result Update | NBFC

Oct 30, 2018

Shriram Transport Fin Co

BUY

CMP

`1,301

Performance Highlights

Target Price

`1,760

Investment Period

12 Months

Particulars (` cr)

2QFY19

1QFY19

% chg (qoq) 2QFY18

% chg (yoy)

NII

2,055

1,881

9.3

1,649

24.6

Sector

NBFC

Pre.Prov. Profit

1,622

1,416

14.5

1,322

22.7

Market Cap (` cr)

25,473

PAT

609

573

6.3

496

22.7

Beta

1.2

Source: Company

52 Week High / Low

1670/898

SHTF reported 2QFY19 PAT of `609cr (up 23% yoy/6% qoq), helped by strong

AUM growth and marginal improvement in NIM. NII increased 25% yoy with

Avg. Daily Volume

1,27,000

reported NIM increased 6bps (8bps qoq) to 7.52%. Operating profit growth was

Face Value (`)

10

healthy at 23% YoY to `1,622cr. Asset quality improved QoQ with Gross Stage 3

BSE Sensex

33,891

ratio falling 40bps QoQ to 8.71% (on AUM) while coverage ratio remained

Nifty

10,198

stable at 34%.

Reuters Code

SRTS.NS

Healthy AUM growth; Stable NIM

Bloomberg Code

SHTF.IN

During the quarter SHTF reported commendable growth of 21%yoy, led by

business loan (105% yoy on low base) and new vehicle (46% yoy). The reported

NIM increased 6bps yoy (8bps qoq), rise in yields (rate hike in June-18) and lower

Shareholding Pattern (%)

CoF on account of change in the borrowing mix. The Cost-income ratio increased

Promoters

26.1

91bps YoY to 22% as the company continued investment into manpower and

MF / Banks / Indian Fls

4.0

branches during the year. Credit cost sequentially increased 50bps to 2.6%, but

FII / NRIs / OCBs

51.2

the management is confident of reducing it to 2.0% over the coming 1-1.5 years.

Indian Public / Others

6.9

On asset quality front, Absolute Gross stage 3 assets declined 1% qoq and similar

qoq decline in Net stage 3 also. The Gross stage 3 ratio declined 40bps qoq to

8.7% (on AUM) while the net stage 3 ratio declined 28bps QoQ to 5.7%.

Abs.(%)

3m 1yr 3yr

Coverage ratio remained stable at 34%.

Sensex

(9.6)

1.9

27.1

SHTF

(20.6)

(4.8)

19.1

On liquidity front, SHTF has `1000cr of liquidity on its balance sheet, in addition

to `2000cr of committed bank lines (equal to one month’s liability payments).

Outlook & Valuation: We expect SHTF’s AUM to grow at CAGR of 20% over

FY18-20E led by stronger CV volume, macro recovery and improving rural

market. The company’s return ration are at decade low levels (RoA/RoE -

3-year price chart

1.9%/13% in FY18) primarily owing to higher credit cost, which we believe to

1,700

normalize FY19E onwards, which would propel RoA/RoE to 2.8%/20.7% in

1,500

1,300

FY20E. At CMP, the stock is trading at 2.1x FY20E ABV and 10x FY20E EPS. We

1,100

recommend a BUY on the stock with a target price of `1,760/-.

900

700

Exhibit 1: Key Financials

Y/E March (` cr)

FY16

FY17

FY18

FY19E

FY20E

NII

5,052

5,561

6,771

8,042

9,702

YoY Growth (%)

32.0

10.1

21.8

18.8

20.6

Source: Company, Angel Research

PAT

1,178

1,257

1,569

2,315

3,284

YoY Growth (%)

(4.8)

6.7

24.8

47.5

41.9

EPS

52

55

69

102

145

Adj Book Value

397

425

460

561

675

Jaikishan J Parmar

P/E

22

20

16

11

8

022 39357600, Extn: 6810

P/Adj.BV

2.8

2.6

2.4

2.0

1.7

ROE (%)

12.2

11.7

13.1

16.6

19.7

ROA (%)

1.9

1.8

1.9

2.4

2.8

Source: Company

Please refer to important disclosures at the end of this report

1

Shriram Transport Fin Co | 2QFY2019 Result Update

Exhibit 1: Quarterly Result Update

Particulars (` cr)

2QFY17

3QFY17

4QFY17

1QFY18

2QFY18

3QFY18

4QFY18

1QFY19

2QFY19

% QoQ % YoY

Total Interest Income

2,689

2,695

2,683

3,116

3,233

3,063

3,271

3,732

3,917

5

21

Interest Expenses

1,336

1,282

1,275

1,283

1,584

1,354

1,463

1,851

1,862

1

18

Net Interest Income (NII)

1,353

1,412

1,409

1,832

1,649

1,709

1,808

1,881

2,055

9

25

% Growth YoY

4

(2)

5

35

17

21

(1)

14

20

44

21

Other Income

17

18

24

22

27

22

172

7

24

229

(10)

Total Income

2,706

2,713

2,707

3,138

3,260

3,085

3,443

3,740

3,942

5

21

Net Income

1,370

1,430

1,433

1,854

1,676

1,731

1,979

1,888

2,080

10

24

Operating Expenses

314

291

290

338

354

383

419

472

458

(3)

29

Employee Expenses

139

131

127

173

164

181

206

225

232

3

42

Other Operating Expenses

175

160

164

165

190

202

213

247

226

(9)

19

Operating Profit

1,056

1,139

1,142

1,516

1,322

1,349

1,560

1,416

1,622

15

23

Provisions

462

611

911

582

567

585

1,367

533

684

28

21

PBT

594

529

231

934

755

763

193

883

938

6

24

Provisions for Tax

206

183

81

238

259

268

49

310

329

6

27

Tax Rate %

35

35

35

26

34

35

25

35

35

(0)

2

PAT

388

346

150

696

496

496

145

573

609

6

23

Asset Quality

GNPA

4,242

4,306

5,408

5,549

5,773

6,046

7,376

7,459

7,749

4

34

NNPA

1,252

1,058

1,659

1,620

1,655

1,751

2,131

2,132

2,278

7

38

Gross NPAs (%)

7

7

8

8

8

8

9

9

9

(21)

71

Net NPAs (%)

2

2

3

2

2

2

3

3

3

1

30

PCR (Calculated, %)

69

74

68

69

70

69

69

69

69

(84)

(96)

Credit Cost (Annualised) AUM

2.5

3.2

4.6

2.9

2.6

2.6

5.7

2.1

2.6

50

(1)

GS 3

8,972

9,191

9,084

9,157

9,092

(1)

(1)

ECL prov stage 3

3,389

3,301

3,286

3,118

3,113

(0)

(6)

Net Stage 3

5,583

5,890

5,799

6,039

5,979

(1)

2

Coverage Ratio Stage 3

38

36

36

34

34

19

(168)

GS 1& 2

73,482

77,282

87,617

91,879

96,173

5

24

ECL prov stage 1& 2

2,148

2,280

2,364

2,341

2,604

11

14

Net Stage 1 & 2

71,336

75,002

85,253

89,538

93,568

5

25

ECL Prov (%) Stage 1&2

3

3

3

3

3

16

(24)

Business Details ()

AUM

75,323

76,281

78,761

81,612

86,357

90,019

95,306

1,00,541

1,04,380

4

21

On book Loans

63,689

64,271

65,463

68,301

71,113

74,884

79,673

82,462

87,815

6

23

Off book (Securitization)

11,634

12,011

13,298

13,311

15,244

15,134

15,633

18,079

16,565

(8)

9

Total Borrowings

51,830

51,130

53,110

55,650

72,970

59,120

63,320

71,860

88,202

23

21

AUM Mix (%)

New CV Loans

10

10

10

10

10

11

11

13

13

0

0

Used CV loans

90

90

87

87

87

86

84

87

87

0

0

Profitability

NIM

7.0

7.2

7.0

7.4

7.5

7.5

7.5

7.4

7.5

8

6

C/I

22.9

20.3

20.3

18.2

21.1

22.1

21.2

25.0

22.0

(300)

89

ROE

14.5

12.5

5.3

24.3

17.1

16.4

4.6

17.2

17.0

(18)

(8)

Source: Company, Angel Research

Oct 30, 201

2

Shriram Transport Fin Co | 2QFY2019 Result Update

Exhibit 2: AUM Break-up

1QFY18

2QFY18

1QFY19

2QFY19

% QoQ

% YoY

New

8,186

8,697

12,140

12,719

5

46

Used

71,957

74,744

83,919

86,057

3

15

Business Loan

1,197

1,615

2,978

3,314

11

105

Working Capital

1,224

1,209

1,895

2,171

15

80

Others

33

92

46

119

159

29

AUM

82,597

86,357

1,00,978

1,04,380

3

21

Source: Company, Angel Research

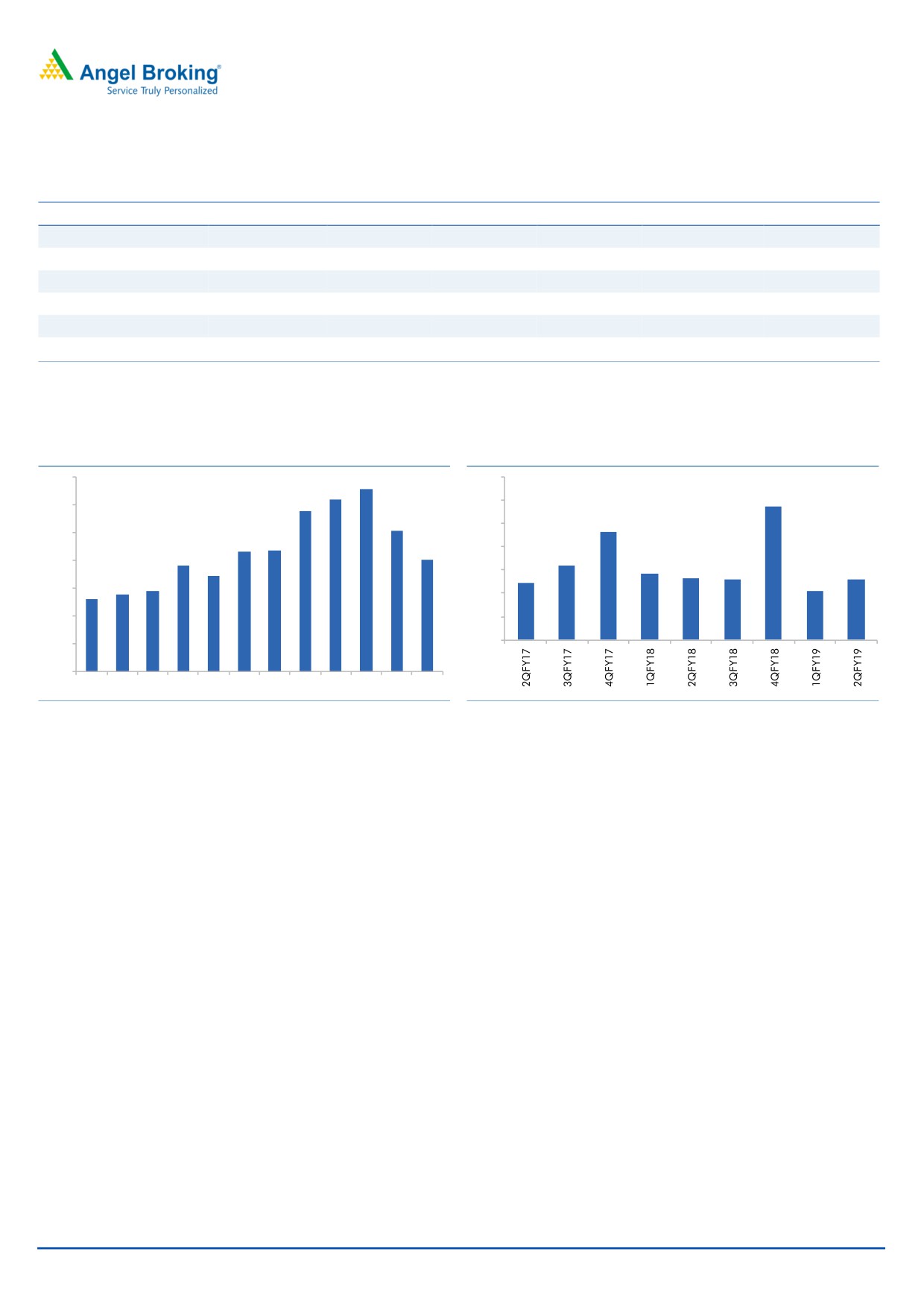

Exhibit 3: Annual trend of credit cost (%)

Exhibit 4: Quarterly trend of credit cost (%)

3.5

3.3

7.0

3.1

5.7

2.9

6.0

3.0

2.5

4.6

5.0

2.5

2.2

2.2

2.0

4.0

1.9

3.2

2.0

1.7

2.9

3.0

2.5

2.6

2.6

2.6

1.4

1.4

2.1

1.5

1.3

2.0

1.0

1.0

-

0.5

-

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18 FY19E FY20E

Source: Company, Angel Research, Note-CC on AUM

Source: Company, Angel Research, Note-CC on AUM

STFC credit cost is continually inching up owing to transition of NPA

recognition from180DPD (Q3FY16) to gradually move to 90DPD in Q4FY18.

Credit cost has increased 50bps sequentially to 2.6% in Q2FY19.Howevertn

management is confident f reducing it to 2% over the coming 1.1.15 years.

During the quartet provision exp increased by 23% qoq(15%-yoy). Out of total

provision of `683 cr in Q2FY19. `60cr was adhoc provision for Kerala.

Outlook & Valuation: We expect SHTF’s AUM to grow at CAGR of 20% over FY18-

20E led by stronger CV volume, macro recovery and improving rural market. The

company’s return ration are at decade low levels (RoA/RoE - 1.9%/13% in FY18)

primarily owing to higher credit cost, which we believe to normalize FY19E

onwards, which would propel RoA/RoE to 2.8%/20.7% in FY20E. At CMP, the stock

is trading at 1.5x FY20E ABV and 8x FY20E EPS. We recommend a BUY on the

stock with a target price of `1,760 (2.7x FY2020E ABV).

Oct 30, 201

3

Shriram Transport Fin Co | 2QFY2019 Result Update

Income Statement

Y/E March ( `cr)

FY15

FY16

FY17

FY18

FY19E FY20E

NII

3,827

5,052

5,561

6,771

8,042

9,702

- YoY Growth (%)

9.5

32.0

10.1

21.8

18.8

20.6

Other Income

428

184

82

248

134

160

- YoY Growth (%)

(6.9)

(57)

(55.5)

202.9

(46.1)

19.7

Operating Income

4,255

5,236

5,643

7,019

8,176

9,862

- YoY Growth (%)

7.6

23.1

7.8

24.4

16.5

20.6

Operating Expenses

1,123

1,347

1,275

1,524

1,764

2,113

- YoY Growth (%)

14.7

20.0

(5.4)

19.6

15.7

19.8

Pre - Provision Profit

3,132

3,888

4,368

5,495

6,412

7,749

- YoY Growth (%)

5.2

24.2

12.3

25.8

16.7

20.9

Prov. & Cont.

1,289

2,107

2,444

3,122

2,905

2,773

- YoY Growth (%)

12.2

63.4

16.0

27.7

(7)

(4.5)

Profit Before Tax

1,842

1,781

1,924

2,373

3,507

4,976

- YoY Growth (%)

0.8

(3.3)

8.0

23.3

47.8

41.9

Prov. for Taxation

605

603

667

804

1,192

1,692

- as a % of PBT

32.8

33.9

34.6

33.9

34.0

34.0

PAT

1,238

1,178

1,257

1,569

2,315

3,284

- YoY Growth (%)

(2.1)

(4.8)

6.7

24.8

47.5

41.9

Balance Sheet

Y/E March ( `cr)

FY16

FY17

FY18

FY19E

FY20E

Share Capital

227

227

227

227

227

Reserve & Surplus

9,927

11,075

12,345

15,072

17,833

Networth

10,154

11,302

12,572

15,299

18,060

Borrowing

49,791

53,110

63,320

75,494

90,007

- YoY Growth (%)

12.5

6.7

19.2

19.2

19.2

Other Liab. & Prov.

8,018

9,998

12,578

14,403

17,849

Total Liabilities

67,963

74,410

88,470

1,05,195

1,25,917

Investment

1,356

1,549

1,480

1,480

1,480

Cash

2,364

4,441

3,638

3,944

4,733

Advance

61,878

65,463

79,673

95,608

1,14,729

- YoY Growth (%)

25.7

5.8

21.7

20.0

20.0

Fixed Asset

101

84

120

144

151

Other Assets

2,264

2,874

3,560

4,020

4,824

Total Asset

67,963

74,410

88,470

1,05,195

1,25,917

Growth (%)

14.6

9.5

18.9

18.9

19.7

Oct 30, 201

4

Shriram Transport Fin Co | 2QFY2019 Result Update

Exhibit 5: Key Ratio

Y/E March

FY16

FY17

FY18

FY19E

FY20E

Profitability ratios (%)

NIMs

8.7

8.5

9.1

9.0

9.1

Cost to Income Ratio

25.7

22.6

21.7

21.6

21.4

RoA

1.9

1.8

1.9

2.4

2.8

RoE

12.2

11.7

13.1

16.6

19.7

Asset Quality (%)

Gross NPAs (%)

6.20

8.20

9.15

9.0

8.0

GNPA Amt

3,870

5,408

7,376

8,605

9,178

Net NPAs

1.9

2.7

2.83

2.7

2.4

NPA Amt

1,144

1,659

2,131

2,581

2,753

Provision Coverage

69.4

67.1

69.1

70.0

70.0

Credit Cost (AUM)

2.9

3.1

3.3

2.5

2.0

Per Share Data (`)

EPS

52

55

69

102

145

ABVPS

397

425

460

561

675

DPS

10

10

11

16

23

BVPS

448

498

554

674

796

Valuation Ratios

PER (x)

21.6

20.3

16.3

11.0

7.8

P/ABVPS (x)

2.8

2.6

2.4

2.0

1.7

P/BVPS

2.5

2.3

2.0

1.7

1.4

Dividend Yield

0.9

0.9

1.0

1.4

2.0

DuPont Analysis

NII

7.9

7.8

8.3

8.3

8.4

(-) Prov. Exp.

3.3

3.4

3.8

3.0

2.4

Adj. NII

4.6

4.4

4.5

5.3

6.0

Other Inc.

0.3

0.1

0.3

0.1

0.1

Op. Inc.

4.9

4.5

4.8

5.4

6.1

Opex

2.1

1.8

1.9

1.8

1.8

PBT

2.8

2.7

2.9

3.6

4.3

Taxes

0.9

0.9

1.0

1.2

1.5

RoA

1.9

1.8

1.9

2.4

2.8

Leverage

6.6

6.6

6.8

6.9

6.9

RoE

12.2

11.7

13.1

16.6

19.7

Source: Company

Oct 30, 201

5

Shriram Transport Fin Co | 2QFY2019 Result Update

Research Team Tel: 022 - 39357800

DISCLAIMER:

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National

Commodity & Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and

Investment Adviser with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for

accessing /dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-

managed public offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any

investment decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this

document should make such investigations as they deem necessary to arrive at an independent evaluation of an investment in

the securities of the companies referred to in this document (including the merits and risks involved), and should consult their

own advisors to determine the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions

and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a

company's fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our

website to evaluate the contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other

reliable sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as

such, as this document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be

in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information

contained in this report. Angel Broking Limited has not independently verified all the information contained within this

document. Accordingly, we cannot testify, nor make any representation or warranty, express or implied, to the accuracy,

contents or data contained within this document. While Angel Broking Limited endeavors to update on a reasonable basis the

information discussed in this material, there may be regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be

reproduced, redistributed or passed on, directly or indirectly.

Disclosure of Interest Statement

Shriram Transport Fin

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

Oct 30, 201

6